Health insurance costs, visualized

Shopping for health insurance is a confusing experience. There’s a new vocabulary to learn, and it’s not obvious what the most important decisions are. A typical “summary of benefits” for a plan runs nine pages, and comparing it to other plans is difficult. I saw a lot of complexity regarding the types of health care services that are within the scope of a particular health insurance plan, which ones might apply to me and my family, and how much those services cost.

There are a lot of different variables:

- In-network vs. out-of-network

- Monthly cost of “premiums”

- A plan’s “deductible”

- Per-visit costs

- Per-test costs (and per-test-category-per-day costs!)

- Co-insurance amounts

- Facility fees

- The “allowed amount”

- etc.

An example of a summary of benefits from Tufts Health Plan is here.

Simplifying

There is a simpler way to look at this. Fundamentally, the goal of health insurance is to distribute the financial risk of health care costs across a population. Some people will get sick and require expensive treatment, others will remain healthy. Having health insurance allows me to limit my financial downside if I get very sick. I pay for this assurance. [1]

There are a few key elements of a health insurance plan:

- Distribution of financial risk. As an example, let’s say that there’s a 1% chance of getting cancer. The cost of curing this cancer is $1,000,000. A group of 100 people go to an insurance company and each pay $10,010. When one of them gets sick, there’s 100×$10,000 = $1,000,000 available to pay for the cure. (The insurance company makes $1,000 for collecting the money, etc.)

- Encouragement of preventative treatment. Preventing problems is much less expensive than treating them. Lung cancer is somewhat preventable, so smokers pay more than non-smokers for health insurance.

- Discouragement of unnecesary treatment. When I’m paying for health care treatment, I’m more likely to ask myself whether it’s necessary or not. The “deductible” and “co-insurance” are aimed at this goal.

- Flexible financing. There are tradeoffs between a high monthly payment (with few costs beyond that), and a high deductible plan (with low monthly payments).

Visualizing

Comparing different health plans can be boiled down to four numbers:

- The monthly premium

- The “deductible,” or the amount below which you pay all health care costs

- The “co-insurance” rate, or the percentage of health care costs you pay above your deductible

- The “out-of-pocket maximum,” which is the most you’ll pay for health care costs. This typically is in addition to your monthly premium.

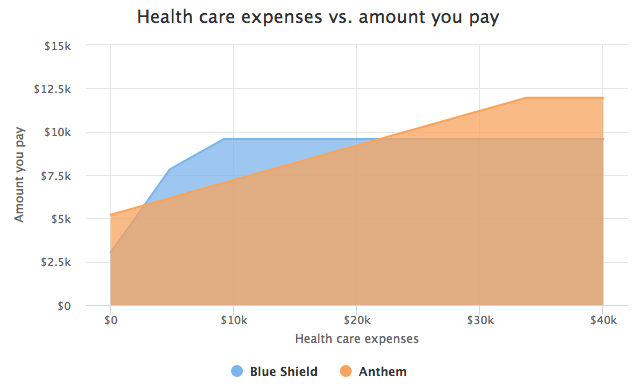

The graph below compares two health plans quoted via the California health exchange [2]:

At the extreme right of the graph, with high health care expenses, both plans provide a cap on how much you would pay. That’s the limit to financial downside that I mentioned above. Those maximum amounts remain the same even if treatment costs millions of dollars.

Choosing

Choosing a health insurance plan, then, is more about matching the shape of the graph above with (1) the treatment you expect to need and (2) your month-to-month financial situation. If you’re young and healthy, and don’t foresee any medical treatment, the Blue Shield plan will be less expensive. Between $5,000 and $20,000 of health care expenses, the Anthem plan will cost less, and will also be less uneven (a flat 20% share, as opposed to a complicated deductible + coinsurance calculation). And above $20,000 of medical expenses, the difference hardly matters - at that point, managing a severe medical condition will be more important than the 15% difference in cost.

Here is a spreadsheet that might help you to evaluate different plans.

Closing thought

One last, very important item - tucked away in a dense “Summary of Benefits and Coverage,” is this note:

Be aware, your participating doctor or hospital may use a non-participating provider for some services.

If you need medical treatment, it is critical that you or your family continuously ask the question: “Is this treatment/service/specialist in-network for my insurance?” Otherwise, a surprise bill might arrive in the mail, and the cap on expenses (protection against financial downside) will not apply.

Notes:

- There is a more complex discussion of health care pricing, government subsidies, and the problems of an uninsured population that I’ll leave aside for now!

The four key numbers for these plans are:

Blue Shield Bronze Anthem Gold Monthly premiums $252 $434 Deductible $4,800 $0 Co-insurance 40% 20% Out-of-pocket maximum $6,550 $6,750